Warsh Reshapes Federal Reserve Communications With Risky New Approach/ Newslooks/ WASHINGTON/ J. Mansour/ Morning Edition/ Federal Reserve Chair Kevin Warsh is reducing the central bank’s communication and guidance to financial markets. Economists warn the move could increase market volatility and potentially push borrowing costs higher. Warsh argues investors should rely more on economic data and less on Fed signals when forecasting policy decisions.

Kevin Warsh Federal Reserve Strategy Quick Looks

- Warsh shortened the Fed’s policy statement dramatically.

- The new Fed chair removed forward guidance from interest-rate announcements.

- Markets reacted with volatility following the Fed meeting.

- Treasury yields rose sharply after Warsh’s first press conference.

- Analysts say less guidance may lead to higher borrowing costs.

- Warsh has cited former Fed Chair Alan Greenspan as a model.

- Five task forces will review key areas of Fed operations.

- Critics say less guidance requires clearer contingency plans.

- Supporters argue markets have become too dependent on Fed messaging.

- The strategy marks one of the biggest shifts in Fed communications in decades.

Deep Look

Kevin Warsh Begins Reversing Decades of Federal Reserve Transparency

For years, the Federal Reserve steadily transformed itself from a secretive institution into one that openly communicated its goals, economic outlook, and future policy intentions. Under new Chair Kevin Warsh, however, that trend may be changing.

During his first press conference as head of the central bank, Warsh made it clear that he intends to reduce the amount of guidance the Fed provides to financial markets. The move reflects his belief that investors have become overly reliant on signals from policymakers rather than analyzing economic conditions independently.

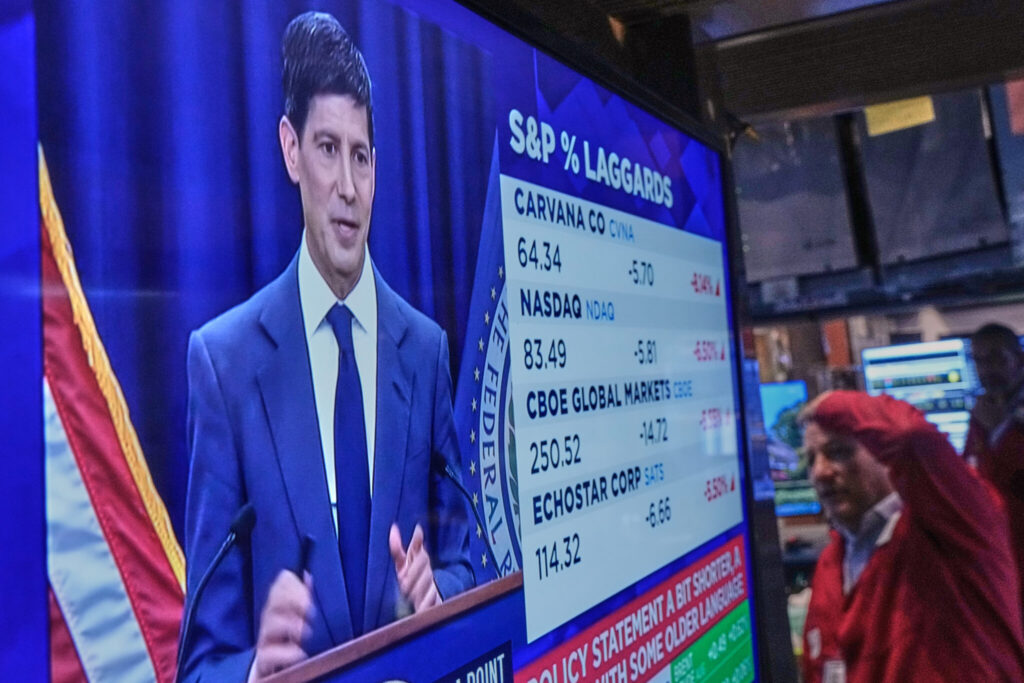

One of Warsh’s first actions was dramatically shortening the Federal Reserve’s policy statement. The announcement following the latest interest-rate decision was cut to just 132 words, down from 341 words in April. The revised statement intentionally avoided offering clues about future rate decisions.

Warsh emphasized that the omission was deliberate, signaling a departure from the practice known as “forward guidance,” where the Fed offers hints about its likely policy path.

Markets React to the New Approach

Investors responded immediately to the Fed’s shift in communication style.

Financial markets experienced significant swings following Wednesday’s statement and Warsh’s remarks. Treasury yields climbed while stocks moved lower, reflecting uncertainty about the central bank’s future plans.

Economists note that forward guidance has traditionally helped reduce uncertainty and stabilize market expectations.

“Forward guidance in general has served to suppress volatility and anchor market expectations,” said George Pearkes, global macro strategist at Bespoke Investment Group. “And that has led to lower borrowing rates, relative to alternatives.”

Pearkes added that the impact on consumers may ultimately be limited, although mortgage rates could end up roughly a quarter-percentage point higher than they otherwise would have been.

The yield on the benchmark 10-year Treasury note jumped after the announcement, while the two-year Treasury yield, which is closely tied to expectations for Fed policy, also moved higher. Stocks sold off as investors adjusted to the possibility of less visibility into future interest-rate decisions.

A Return to the Greenspan Era?

Many analysts believe Warsh is drawing inspiration from former Federal Reserve Chair Alan Greenspan, who led the central bank from 1987 through 2005.

Greenspan was known for his cautious and often cryptic public comments, leaving markets to interpret economic signals without extensive guidance from policymakers.

The first post-meeting Fed statement was introduced during Greenspan’s tenure in February 1994. At the time, the Fed surprised investors by raising rates for the first time in five years, causing a sharp market reaction.

Warsh appears interested in restoring some of that uncertainty.

His broader reform agenda extends beyond policy statements. The Fed is launching five separate task forces to review communications practices, balance sheet management, economic data collection, artificial intelligence’s impact on productivity and employment, and the frameworks used to assess inflation.

The communications review could potentially lead to changes in quarterly economic forecasts and even the frequency or format of press conferences.

“This is a big change in how the Fed has conducted itself since the (2008-2009) global financial crisis,” Matthew Luzzetti, chief U.S. economist at Deutsche Bank, said. “Since then there has been a one-way train to greater communication, more transparency, and more forward guidance. Warsh has now put that train in reverse.”

Why Previous Fed Leaders Embraced Forward Guidance

Former Fed leaders, especially Ben Bernanke and Jerome Powell, viewed communication as a powerful policy tool.

Because the Fed directly controls only short-term interest rates, policymakers have often used guidance to influence longer-term borrowing costs by shaping investor expectations.

When markets believe the Fed will raise or lower rates in the future, bond yields often move before the central bank actually takes action. This allows policymakers to affect economic conditions more efficiently.

Warsh, however, believes markets should play a larger role in interpreting economic developments.

Rather than relying on official forecasts, investors should draw conclusions from incoming data and market conditions.

“Financial market prices are probably the most important source of information to guide central bankers,” Warsh said at Wednesday’s news conference.

Critics Want More Clarity

Not everyone agrees with the new strategy.

David Andolfatto, an economics professor at the University of Miami and former economist at the Federal Reserve Bank of St. Louis, said forward guidance certainly has weaknesses because unexpected events can quickly make previous forecasts obsolete.

Major disruptions such as geopolitical conflicts, pandemics, or inflation shocks can force policymakers to change direction rapidly.

Still, Andolfatto believes Warsh should offer a clearer framework explaining how the Fed would respond under different scenarios.

“I’m with him on dispensing with forward guidance, but you have to replace it with a contingency plan,” Andolfatto said. “It’s not enough to say, trust me, we’ll keep inflation at target.”

More Attention on Regional Fed Officials

One unintended consequence of reducing guidance from the chair may be increased attention on other Federal Reserve officials.

Without clear signals from the top, investors may look more closely at speeches and comments from regional Federal Reserve bank presidents and members of the Board of Governors for clues about future policy decisions.

Pearkes noted that this could actually increase the influence of the broader Federal Open Market Committee, whose members regularly provide public commentary on economic conditions.

The result may be a more fragmented information environment where markets analyze multiple voices rather than focusing primarily on the Fed chair.

A Major Test Still Lies Ahead

The ultimate challenge for Warsh’s strategy may emerge during the next financial crisis or economic downturn.

During periods of extreme uncertainty, forward guidance has often been used as a stabilizing tool to reassure investors and calm markets. Economists say it remains unclear whether a less communicative Federal Reserve can maintain confidence during future crises.

“Whether it will stand the test of time and he will behave this way for five years is a very different question, but one that we’re going to have to wait for events to unfold to get an answer to,” Pearkes said.

You must Register or Login to post a comment.